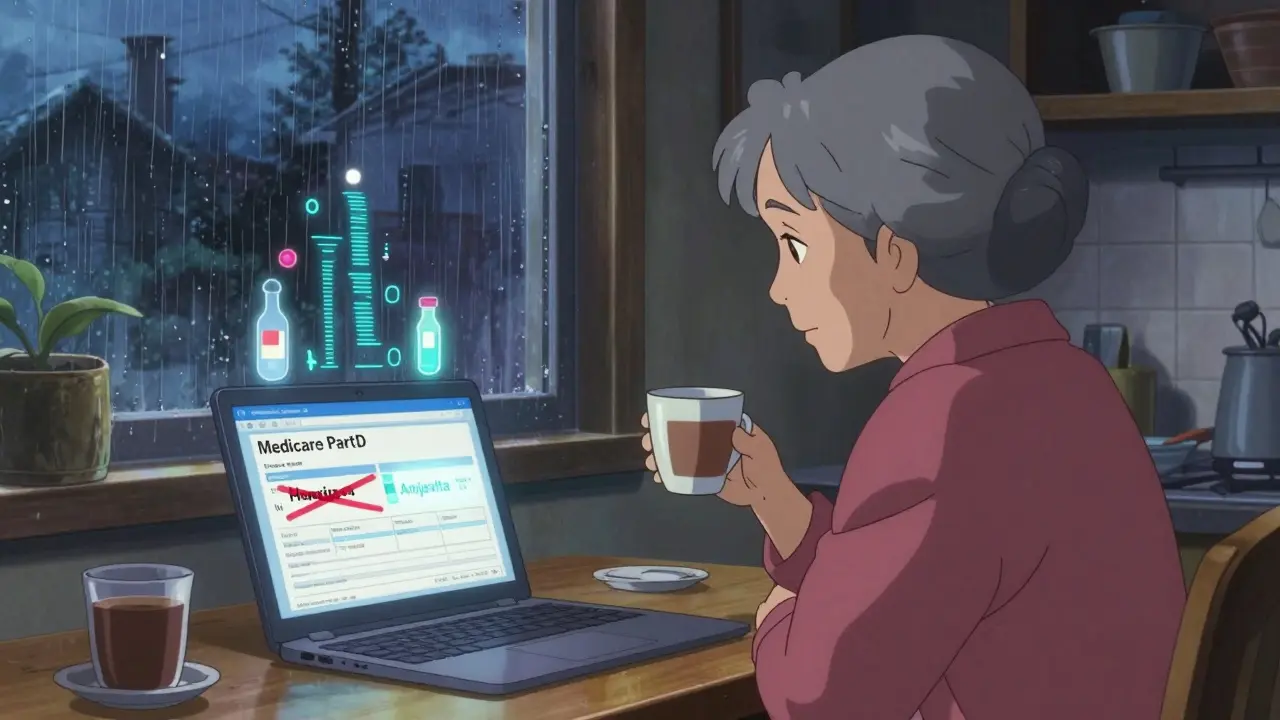

Every January, millions of people on Medicare Part D wake up to find their prescriptions have changed - not because their doctor switched them, but because their insurance plan did. If you’re taking a brand-name drug like Humira, Humalog, or Stelara, you might be surprised to see your copay jump from $35 to $113 overnight. Or worse, your medication might not be covered at all. This isn’t a mistake. It’s a formulary update.

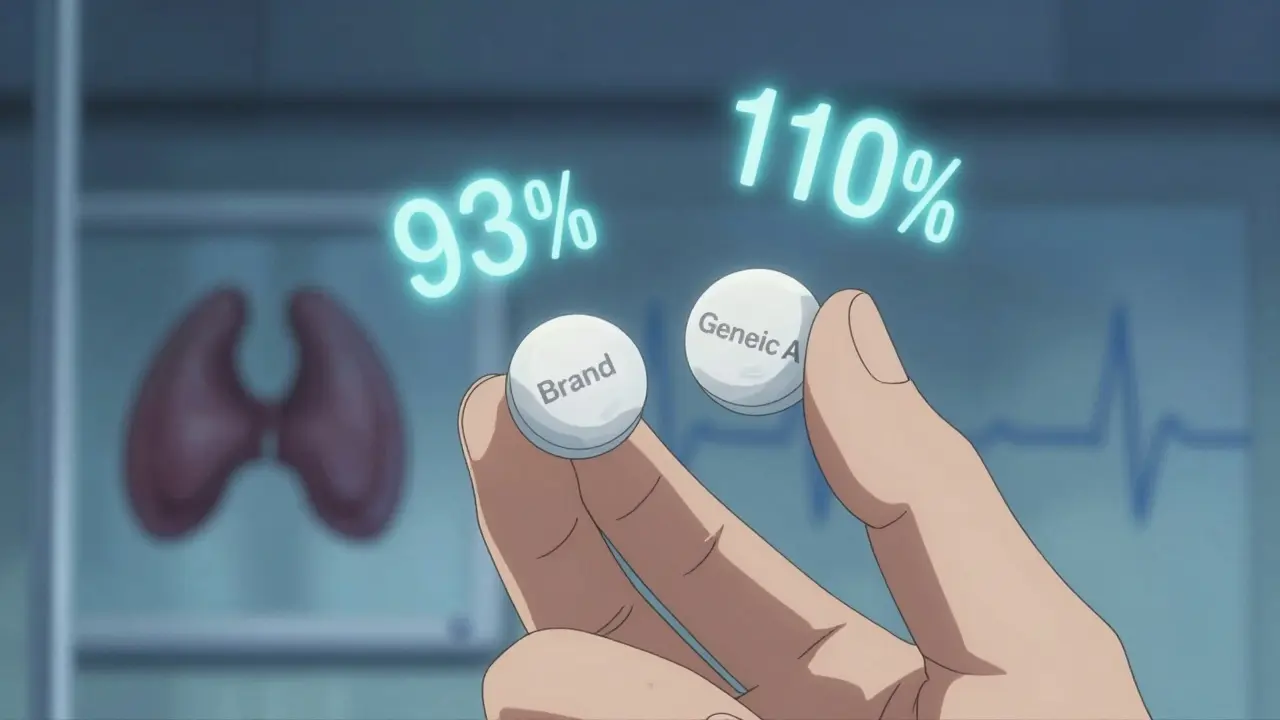

Okay but let’s be real - if your PBM is pushing Amjevita over Humira and you’re not experiencing a single adverse event, you’re literally saving $450/month. 🤑 That’s a vacation. That’s groceries. That’s not ‘switching,’ it’s financial liberation. The system’s rigged, but this? This is how you hack it. 📉💉 #BiosimilarsAreNotScary

Every single one of us deserves access to life-sustaining medication - not a spreadsheet-driven gamble. This isn’t just about cost; it’s about dignity. If your insurer thinks a biosimilar is ‘good enough’ without consulting your rheumatologist, they’re failing you. But here’s the hope: YOU have power. Know your rights. File exceptions. Speak up. You are not invisible.

People complain about formulary changes like it’s a conspiracy. Newsflash: insurance is a business. If you’re on a $700/month drug when a $350 alternative exists, you’re being subsidized by everyone else’s premiums. Stop acting like your brand-name drug is a constitutional right. Be grateful you’re not paying $1,200 like in 2018.

I switched from Humira to Amjevita last year. My skin cleared up. My joints stopped screaming. My bank account stopped crying. 😭💸 I cried when I saw the $48 copay. I cried again when I bought a new pair of boots with the savings. THIS IS WHAT LIBERATION LOOKS LIKE. 🙌

Wow. So we’re supposed to be thrilled that corporations are forcing us to take ‘near-identical’ drugs because they’re cheaper? Let me guess - the PBM execs still get their $12M bonuses. Meanwhile, I’m supposed to trust a ‘biosimilar’ that’s been on the market for 18 months? Please. This isn’t progress. It’s corporate coercion dressed in healthcare jargon.

Why are we letting foreign pharmaceutical companies dictate our medicine? Biosimilars are mostly made overseas. We’re outsourcing our health security. If we had real domestic manufacturing, we wouldn’t be at the mercy of these PBMs. This isn’t healthcare reform - it’s economic surrender.

Thank you for this comprehensive breakdown. The formulary change timeline and exception request thresholds are critical information that too many patients overlook. I’ve shared this with my clinic’s patient education portal. Knowledge is the first line of defense.

You frame this as a battle between patients and insurers, but the real villain is the FDA’s regulatory inertia. If they’d fast-tracked interchangeable biosimilars five years ago, we wouldn’t be in this limbo. And let’s not pretend the drug manufacturers aren’t lobbying to delay generic entry - they’re the ones who priced Humira at $700/month in the first place. The system is a pyramid scheme with patients at the bottom.

My dad got switched from Stelara to a biosimilar. He had a severe flare-up. Took 12 days to get an exception approved. He was hospitalized. The insurer didn’t care. They just sent a form. This isn’t ‘smart cost control.’ It’s medical negligence masked as policy.

Listen - I’ve been on biologics for 14 years. I’ve been switched three times. The first two? Disaster. The third? Amjevita. Zero side effects. Same results. What changed? My mindset. I stopped seeing it as a downgrade and started seeing it as an upgrade in affordability. You don’t have to fight every battle. Pick your wars. And sometimes, the cheaper version is just… fine. Better yet - it’s sustainable.

Wait - so you’re telling me the IRA didn’t cap insulin at $35 for everyone? Why are we still seeing $113 copays? This whole post feels like a PBM ad. If the government negotiated prices, why are PBMs still controlling formularies? You’re missing the point: the problem isn’t the switch - it’s the lack of true price transparency. Fix the root, not the symptom.